# Reflation nation? This time, post-crisis tailwinds favor banks, and the economy

Table of Contents

“#

Reflation nation? This time, post-crisis tailwinds favor banks, and the economy

”

This crisis wasn’t like the 2008 subprime meltdown, and the recovery won’t be either

A decade ago, banks were at the heart of the financial crisis that led to the Great Recession. Lenders like banks enabled the mortgage market froth that brought the financial system to its knees, and after the bubble burst, they were dogged for years by slack demand, stricter regulation, and low interest rates.

Things couldn’t be more different now. Banks were arguably overcapitalized when the corona-crisis erupted, and they made it through the crisis better than anyone could have hoped. Now they look set to ride a historic rebound in lockstep with the economy, instead of being an albatross around its neck.

The worst fears about unemployment weren’t realized, Lerner said in an interview, and defaults have stayed relatively low thanks to massive fiscal and monetary relief, and households have used their stimulus money and time under lockdown to pay down debt and build up their savings.

As a result, a “spring-loaded” economy is likely to emerge in the vaccinated world, he believes. After a year inside, households have pent-up consumption demand, including for big-ticket items like home appliances, juiced by fiscal stimulus payments.

Similarly, said Diane Jaffee, senior portfolio manager at TCW, banks went into the downturn with huge amounts of reserves. In fact, just before the pandemic, a new regulation went into effect, requiring lenders to hold even more on their books.

And throughout 2020, even as the worst-case scenarios dreamed up in the nightmarish early days of the pandemic never came to pass. “Literally, we were expecting 25% unemployment!” Jaffee said. But banks have carried on, putting aside small amounts of fee income that they’ve generated from making loans through the government stimulus programs.

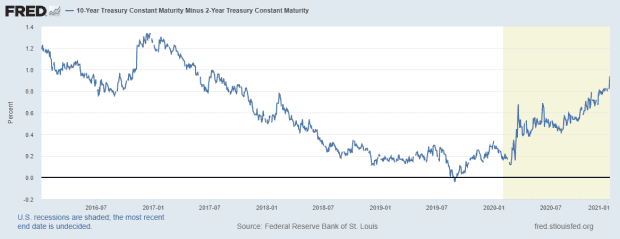

Perhaps even more important than the macroeconomic backdrop may be the market one. After years of headfakes, 2021 may be the year banks finally have interest rates on their side.

Not only is the yield curve steepening, extending the differential between rates at which banks borrow and lend, but with the 10-year Treasury note

TMUBMUSD10Y,

consistently a bit higher than it had been, “the banks start showing stability in net interest income,” Jaffee said. “They’re not just continuously losing money. They don’t have to keep massive cost-cutting just to fight off losses.”

In fact, the country’s biggest bank, JPMorgan Chase & Co.,

JPM,

reported “historic” margins in its third quarter, Jaffee noted, including a 19% return on tangible common equity. It was a “drop-the-mic moment,” she said.

It may also be the year the decades-long bond bull market comes to an end. If bond prices fall, and yields rise, corporate issuers are more likely to turn to banks for loans to meet their financing needs, Jaffee thinks.

JPMorgan will be the first company to kick off Q4 earnings next Friday, followed by Wells Fargo & Co.

WFC,

Analysts haven’t yet released specific earnings estimates, but their initial research is bullish.

“Even after the ‘blue wave’ rip, we believe banks’ relative PEs remain attractive and a case for absolute P/E expansion exists,” Jefferies analysts wrote on Thursday. The Invesco KBW Bank ETF

KBWB,

which tracks the sector closely, has gained more than 11% over the past month as a Democratic sweep of Congress and the White House appeared to grow more likely. November’s 17.6% gain for the fund was its best on record, back to 2012, and the best since 2009 for a broader financial-sector ETF.

XLF,

“An eventual turn in loan growth could join strong deposit growth, better cost control and a restart of buybacks as positives,” the Jefferies analysts concluded.

Jaffee agrees. “I feel very, very confident that banks can continue to pay, and even raise, their dividends,” she told MarketWatch.

Looking to the week ahead, investors will get a report on U.S. inflation in December on Wednesday, when the government releases CPI figures. December retail sales numbers and a slew of manufacturing data will also be published Friday.

Last week, the Dow jones Industrial Average

DJIA,

gained 1.6%, the S&P 500

SPX,

rose 1.8%, and the Nasdaq Composite

COMP,

added 2.4% with the indices all closing at new record highs.

Read next: What will 2021 bring for ETFs?

If you liked the article, do not forget to share it with your friends. Follow us on Google News too, click on the star and choose us from your favorites.

For forums sites go to Forum.BuradaBiliyorum.Com

If you want to read more News articles, you can visit our News category.